Greece, Greece, Greece… all types of economists, political analysts, simply dilettantes, and pseudo specialists are trying to comment on the issue of sovereign debt, Eurozone and the role of Greece in this mess. So I think it is time for us, accountants and auditors to make our pedantic and diligent (as we always do ;) contribution to process of pointing finger at Greece

I have been recently interested in IFRS adoption in different countries and implications of this rather painful process. There are remarkable research papers dedicated to this topic, among which is study by Siqi Li (2010), who analyses impact of IFRS implementation on the cost of equity capital in Europe. I am going to use his analysis to raise some issues about Greece

Lots of Requirements and No Enforcement

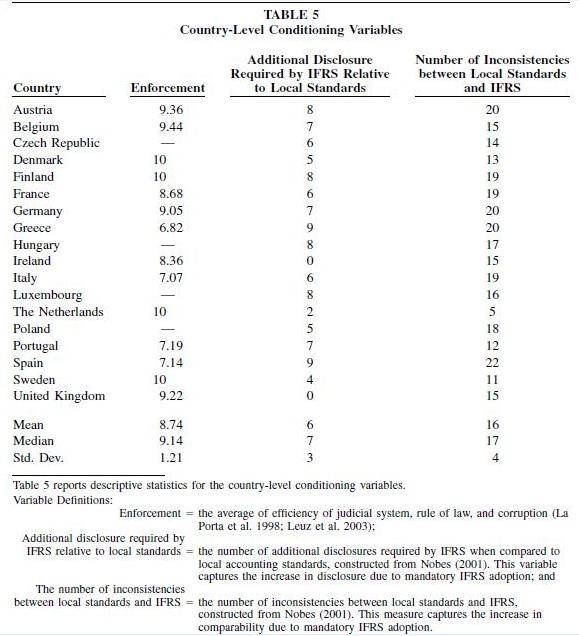

The author of research took into consideration the fact that effective implementation of IFRS depends on country’s institutional arrangements. In other words, benefits from mandatory IFRS adoption in terms of reduction in the cost of equity are expected to be sensitive to whether the new rules are effectively enforced (Li 2010). So, the scholar compared the European countries using such variables as law enforcement (utilizing studies by La Porta et al. (1998); Leuz et al. (2003)), additional disclosures and inconsistencies in standards. This interesting and appealing analysis was presented in Table 5 of his study, which is attached to this post.

Following observations could be made from this table.

First, the best “mutual friends”, Germany and Greece Greece Spain

Second, considering the number of additional disclosures required per IFRS, Greece as well as Spain Germany Poland and Czech Republic

Finally, according to the table the worst enforcement ratings belong to Greece , Italy , Spain , and Portugal

But what can we infer from Greece

This pattern of reasoning might leads us to the same conclusion regarding Greek tax system. As my Greek acquaintances evidence that the tax and legal system in Greece

Quite another issue is the level of indebtedness of the Greek private businesses, particularly banks. Given the information above, can we rely on their IFRS financial statements and do they reflect actual financial position of businesses?

By the way

|

| Kebab mix |

By the way, I do not have anything against Greece

References

La Porta, R., F. Lopez-de-Silanes, A. Shleifer, and R. Vishny. 1998. Law and finance. The Journal of Political Economy 106 (6): 1113–1155.

Leuz, C., D. Nanda, and P. Wysocki. 2003. Earnings management and investor protection: An international comparison. Journal of Financial Economics 69 (3): 505–527.

Li, S. 2010. Does Mandatory Adoption of International Financial Reporting Standards in the European Union Reduce the Cost of Equity Capital. The Accounting Review 85 (2): 607-636

Nobes, C., ed. 2001. GAAP 2001: A Survey of National Accounting Rules Benchmarked Against International Accounting Standards by Andersen, BDO, Deloitte Touche Tohmatsu, Ernst & Young, Grant Thornton, KPMG, PricewaterhouseCoopers. New York , NY